Keep Calm and Stay Invested. History Suggests Patience During Geopolitical Uncertainty

- Mar 2

- 5 min read

Broadening Market Leadership Persists in February

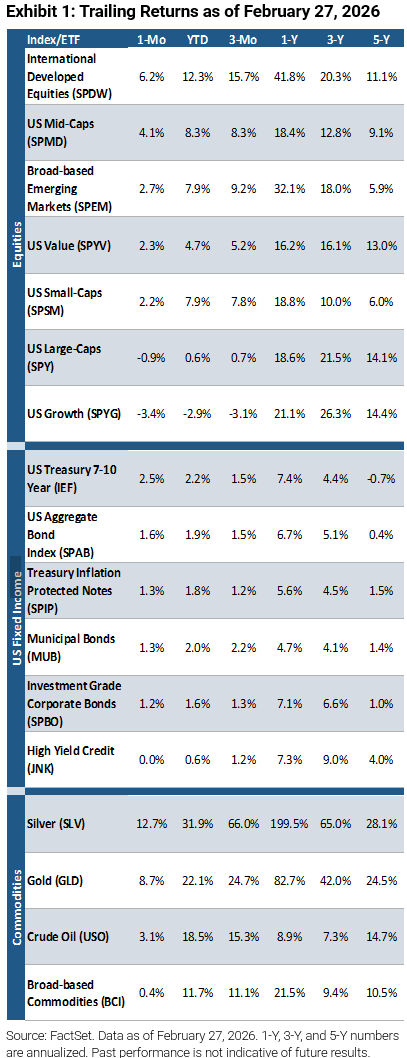

Amid heightened scrutiny of AI-related capex, geopolitical tensions, and a hotter-than-expected inflation report late in the month, US large-cap equities came under pressure in February, with the Nasdaq 100 and S&P 500 declining 2.3% and 0.8%, respectively. However, market leadership continued to broaden beyond mega-caps, as the S&P 500 Equal Weight Index (+3.6%) outperformed its market-cap-weighted counterpart. International developed equities (+6.2%) led gains, followed by US mid-caps (+4.1%) and emerging market equities (+2.7%). Bonds mostly fared well as 7-10 year US Treasuries rose 2.5%, the US Aggregate Bond Index gained 1.6%, and Treasury Inflation Protected Notes increased 1.3%. Commodities produced positive returns as silver was up 12.7%, gold gained 8.7%, crude oil rose 3.1%, and broad-based commodities increased 0.4%.

Fed Likely to Hold Rates Steady in March

Federal Reserve officials appeared to enter February with the intention of holding rates steady for the upcoming March FOMC meeting, and recent data are likely to reinforce that view. January’s Nonfarm Payrolls report came in stronger than expected, with a 130,000 increase versus the forecast of 70,000, while the unemployment rate edged down from 4.4% to 4.3%. Moreover, Friday’s inflation data showed that Core PPI (Producer Price Index, excluding food and energy) rose 0.8% month-over-month versus the 0.3% consensus, marking the highest monthly increase since March 2022, and 3.6% year-over-year. This elevated reading underscores persistent inflation pressures and provides the Fed additional reason to remain cautious about easing. Later in the month, a key development came with the Supreme Court’s tariff ruling. On February 20th, the Court ruled 6-3 that former President Trump had exceeded his authority under the 1977 International Emergency Economic Powers Act. The administration quickly shifted to Section 122 of the Trade Act of 1974, using its “balance-of-payments” provision to reimpose a temporary global tariff, starting at 10% and later raised to the statutory 15% maximum. Looking ahead, markets are pricing in a 94% probability of holding rates steady at the March meeting.

GDP Growth Slows in Q4 2025 Amid Shutdown

US GDP growth eased at the end of 2025, with real GDP rising 1.4% annualized in Q4, below the 2.0% estimate and down from 4.4% in Q3. The moderation reflected several factors. Government spending declined, largely due to the effects of the extended federal government shutdown late in the year. Consumer spending, which makes up about 70% of GDP, slowed somewhat compared with earlier quarters, and exports fell, subtracting from overall growth. Investment and household demand provided some offsetting support. Economists generally view the Q4 reading as at least partly temporary and linked to the shutdown, rather than signaling a broad-based slowdown, though it highlighted ongoing vulnerabilities such as softer private demand and external headwinds as the economy entered 2026.

Will AI Capex Investments Drive Returns or Risk?

The Magnificent 7 tech giants have been ramping up AI infrastructure spending, with hyperscaler capex expected to rise roughly 58% in 2026, surpassing $700 billion. Amazon and Meta are expected to see year-over-year declines in free cash flow, while Oracle is also accelerating spending despite facing headwinds as it builds capacity to support AI growth. These investments may be necessary because existing infrastructure cannot handle next-generation AI workloads at full scale, and companies risk falling behind competitors if they do not expand capacity. At the same time, the scale of spending presents challenges. Return on investment remains uncertain, and higher capital outlays are putting pressure on free cash flow, leaving less cash to weather downturns, fund buybacks, or support dividends. Expensive valuations and circular M&A or stock-based deals have increased market caution, contributing to the recent tech selloff as investors reassess the risk-reward of capital-intensive growth names.

Risks of Private Credit Made Visible

Private credit has been in the spotlight this February as the $2 trillion sector grows beyond traditional leveraged buyouts into areas once dominated by banks. For Blue Owl Capital, trouble first surfaced late last year when it limited withdrawals from one of its retail-focused funds. The situation escalated in mid‑February when the firm announced it would sell $1.4 billion of direct lending investments across three of its business development companies, selling the assets at roughly 99.7% of par and returning about 30% of net asset value to investors. At the same time, Blue Owl said it would stop regular quarterly redemptions in its retail fund, moving instead to periodic capital distributions funded by asset sales and loan repayments, effectively ending the semi-liquid structure investors had relied on. The episode highlights a broader risk in private credit since funds invest in long-term, illiquid loans but sometimes promise investors easier access to cash than the underlying assets allow. The stress has rippled across the sector with publicly traded alternative asset managers including Ares, Blackstone, Apollo, and KKR seeing share price declines as investors reassess liquidity, credit quality, and valuations.

Keep Calm and Stay Invested. History Suggests Patience During Geopolitical Uncertainty

Although recent US and Israeli strikes on Iranian sites may unsettle markets in the short term, history suggests equities tend to recover relatively quickly after geopolitical tensions. Since 1940, the S&P 500 has delivered positive returns 67% of the time in the three months following major geopolitical or historical events, and over the subsequent six months, the index has posted a median return of 5.3%, highlighting the market’s resilience. The historical record underscores the importance of staying patient and maintaining a long-term perspective.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in SPYG, SPY, SPYV, SPDW, SPMD, SPSM, SPEM, SPBO, SPAB, MUB, IEF, SPIP, GLD, SLV, USO, BCI, ORCL, META, GOOGL, AMZN, MSFT, BX, OWL, ARES, and KKR on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements

Comments